Financial Analyst Report - Eagers' Increased Stake in BYD Retail Joint Venture

Eagers Boosts Interest in BYD Retail Joint Venture:

Eagers has disclosed its acquisition of an additional 31% stake in EV Dealer Group Pty Ltd, the national retail joint venture for BYD, raising its ownership from 49% to 80%, effective immediately. The transaction, valued at $70 million, is comprised of $50 million in cash and $20 million in Eagers shares, acquired from EVDirect.com. EVDirect.com will retain a 20% stake in the retail joint venture while also holding exclusive distribution rights for BYD in Australia. Eagers has emphasized that this increased interest reinforces its position as the exclusive retail partner for BYD and EVDirect.com in the Australian market, demonstrating its leadership in the transition to new energy and low-emission vehicles.

Modest EPS Upgrades:

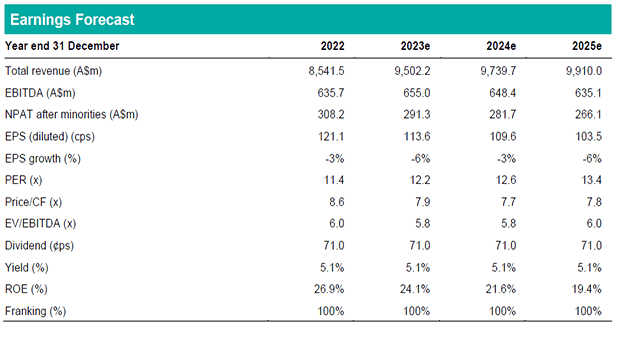

We have revised our forecasts to account for the increased stake in the BYD retail joint venture, although our underlying projections remain unchanged. It's important to note that Eagers already consolidates the joint venture despite initially holding a 49% stake, so the primary change is reflected in the minority interest and NPAT after minorities. Consequently, our revenue and underlying operating PBT forecasts remain unaltered. However, we have made modest upgrades to our EPS forecasts, reflecting increases of 2%, 3%, and 5% for 2023, 2024, and 2025, respectively. We should highlight that our 2023 revenue forecast of $9.5 billion aligns with the guidance range of $9.5 billion to $10.0 billion, with the revenue contribution from the BYD joint venture being a pivotal factor within this range.

Investment View - PT Increased by 1% to $15.15 - Maintain BUY:

Our price target has been adjusted to $15.15/share, representing a marginal 1% increase, taking into account the earnings changes, market developments, and time adjustments. We have also updated the valuations pertaining to the recently announced stake in McMillan Shakespeare, which does not impact our forecasts. Our valuation approach remains consistent, with flat multiples of 12.5x and 6.0x applied to PE ratio and EV/EBITDA valuations, respectively, along with a WACC of 8.9% in the DCF model. Consequently, we maintain our BUY recommendation, given the expected total return of approximately 15%.